One of the most important expenditures the average family

Makes in its lifetime is the purchase of life insurance.

What’s Its Purpose?

First, you must understand the purpose of life insurance.

It is to protect against premature death.

Life insurance does not “insure life” so much as it “protects

Your dependents” from the loss of financial support.

What Are You Paying For?

Second, you must understand what you are paying to protect.

Most people earn from $400,000 to $800,000 during their lifetime.

It is the loss of that earning potential that makes life insurance a

Necessity. Life Insurance is a substitute for the cash and other

Wealth that your family would accumulate if the breadwinner

Were living.

What Should You Buy?

Third, you must understand what kind you should buy.

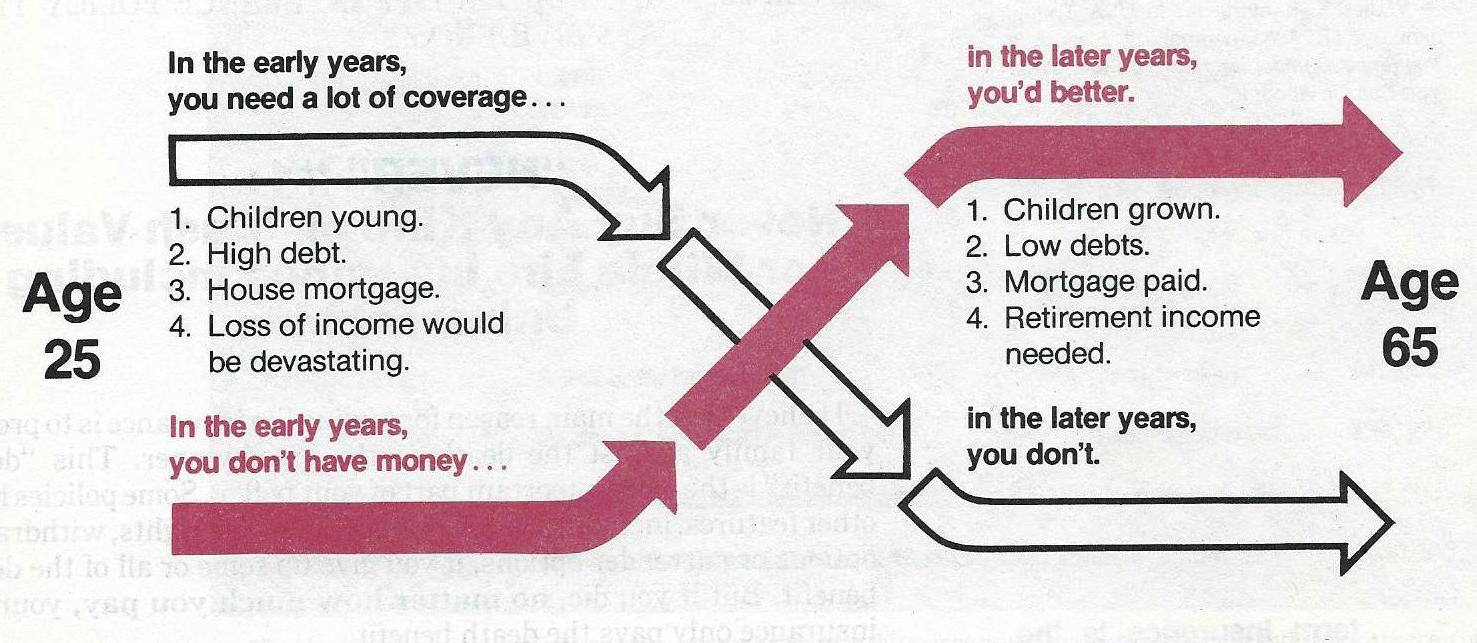

In the early years you need a lot of coverage …

1. Children young.

2. High debt

3. House mortgage.

4. Loss of income would be devastating.

A 20 Year Term Policy on the breadwinner would be sufficient to

cover this scenario.

For example: For a family with two children, $100,000 + $50,000

+ $50,000 equals $200,000 on the breadwinner for adequate protection

for the family. $200,000 of life insurance would give survivors and

annual income of $22,300 per year for 20 years (assuming that the

insurance proceeds earn 10% with annual compounding interest and

that income is payable in monthly installments.)

In the later years you don’t need a lot of coverage …

1. Children grown.

2. Low debts.

3. Mortgage paid.

4. Retirement income needed.

We recommend a Whole Life Policy in this scenario.

For example: $10,000 Natural Death

$10,000 Accidental Death

This would presently cover basic final expenses.

- Art Williams

Edited by Hayden Childs, Agent

“The Grief is bad enough,

Don’t Leave the Burden

To Your Family!”

www.haydenchilds.net

Comments

Post a Comment